Our hotelAVE Hospitality Dashboard 2Q24 is now available!

- Forecasters revised their 2024 full year RevPAR projections down last quarter – all converging around 2.0%. Because the deceleration is ADR related, GOP margin pressures will continue through year end.

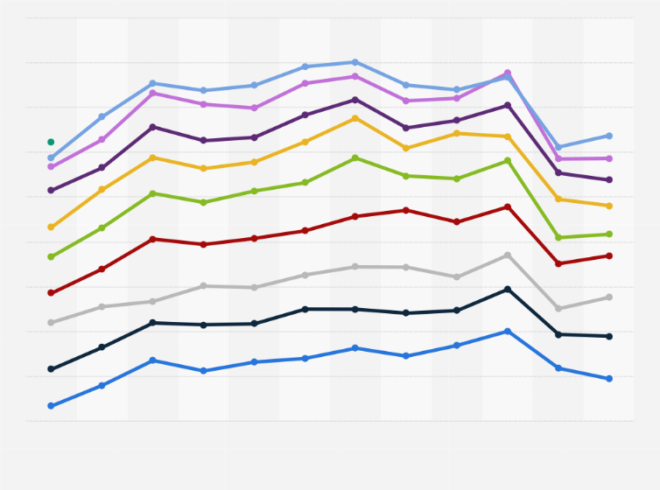

- 2Q24 RevPAR flow to GOP was only 23% in the Top 25 markets; GOP margin decreased 100 bps year over year. Labor cost growth exceeded revenue growth in most markets. Recent REIT earnings calls cited growth in real estate tax and insurance expenses also pressuring EBITDA margins

- Implied cap rates for REITs inched higher in 2Q, more a function of their lower stock prices. Transaction market has been slowed by higher borrowing costs providing fewer data points for investors. Planned renovations (PIP’s), deferred maintenance, and key money blur “true” cap rates.

- Surprisingly, the number of hotel rooms under construction grew quarter over quarter; however, total active pipeline shrank as several projects were abandoned. Despite expensive financing terms for new construction, developers are breaking ground betting on lower interest rates upon completion. Extended stay projects account for more than one third of projects under construction.

- Debt spreads remained steady last quarter, however five- and ten-year financings priced off treasuries benefitted from falling bond rates. SOFR remains pinned to fed funds rate with high expectations for a September cut. CMBS was very active last quarter with borrowing rates 100-300 bps cheaper than debt fund alternatives. Bank financing is easing, but mostly for existing relationships.

Download the full summary to stay up-to-date: hotelAVE Hospitality Dashboard 2Q24