hotelAVE 1Q26 Hospitality Earnings Summary is now available! A glimpse:

hotelAVE 1Q26 Hospitality Earnings Summary is now available! A glimpse:

-

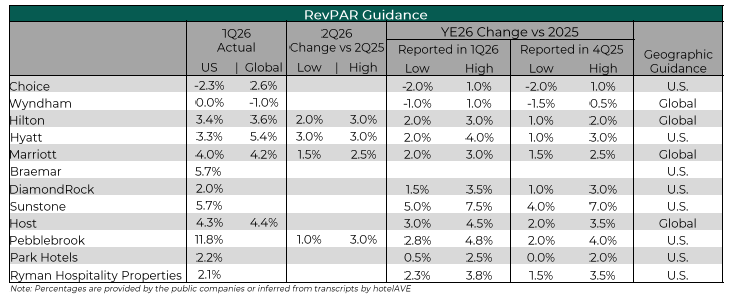

- 1Q26 U.S. RevPAR change reported by the C-Corps was -2.3% to 4.0%; Choice & Wyndham (bell weather for lower end segments) were at the lowest end; HLT, H and MAR were 3.3% to 4.0%. Median REIT RevPAR growth was 4.3%, mostly rate driven

- Everyone (except Choice) raised YE26 guidance by 50 to 100 bps. Mostly driven by strong 1Q; 2H26 outlook was generally unchanged due to the various uncertainties. Choice, Hyatt and Hilton reported select service & lower/mid chain scale improvements

- US Leisure revenue grew 3.5% to 5% in 1Q26. 1Q26 cruise net yields (like RevPAR) grew roundly 2.5%. 1Q26 Airbnb revenue grew 18% (including +9% ADR.) Early Easter, compressed spring breaks in March & shifts from Mexico contributed. Flattish leisure expected for balance of year (except FIFA)

- 1Q26 business transient revenue grew 2.0% to 2.7% for Marriott, Hyatt and Hilton.5; Airline corporate managed revenue grew 13%-16%

- 2026 full year group revenue OTB pacing 4.0% to 7.6% ahead of STLY. Dominantly corporate followed by convention and entertainment. Banquet & catering revenue also grew 3%-6%

- 1Q26 REIT EBITDA margins improved by a (strait line) average of 172 bps, driven by strong RevPAR growth, wage productivity gains, and disciplined expense control

- Capital deployment continues: Park sold 2 non-core hotels YTD; renovations underway at Royal Palm (Park), Gaylord Texan (Ryman), and storm repairs at Wailea Beach (Sunstone)

Download the full summary to stay up-to-date: hotelAVE 1Q26 Hospitality Earnings Summary