Hotel management agreements formalize the contract made between the hotel owner and the operator. They document the requirements, conditions and expectations placed on each party involved. Performance tests figure prominently among these. They are included in hotel management agreements to protect an owner’s investment by allowing the owner to terminate the agreement in the event of poor performance by the operator.

It is essential that performance tests support both operators’ and owners’ needs in order for a hotel to succeed over the mid and long terms. An owner finances a hotel, through raised capital and bank loans, based on the expectation that the property will generate a certain baseline profit – these expectations are the owner’s return requirements on investment. If the hotel fails to perform as expected, the owner’s ability to pay investors and debt service and to invest further in the property is jeopardized. When that performance is inconsistent with the market or effective execution, the only remedy is termination of the operator.

A performance test that supports the expected earnings furthers both the owners’ and operators’ interests. It is essential that the test specified in a hotel management agreement defines a performance threshold that allows the owner to achieve the following:

i) the required stabilized yield on cost or total capitalization;

ii) to pay debt service; or

iii) if those return requirements are not met, allows the owner to terminate the agreement with the operator.

While poor performance should be defined as below-market returns or the inability to pay debt service, the industry typically uses an antiquated, operator-favored methodology that is based on RevPAR penetration and variances from the annual budget.

This is unfortunate, because the old-school method for determining performance frequently creates misalignment between the operator’s and owner’s needs and negates the intended purpose of the test.

Current performance test structure

The standard performance test in most hotel management agreements is two pronged. The performance test proposed by many operators includes two conditions:

1) the hotel must attain a specific revenue per available room (RevPAR) index of an exact competitive set; and

2) the hotel must achieve a gross operating profit (GOP) that is a specific percentage of the budgeted GOP for the year. The operator’s purpose for having two prongs is to provide protection against factors that are out of their control, such as an economic downturn. Failure of the GOP condition due to an economic downturn will be protected by the RevPAR index condition because this condition is not impacted by such an event.

Furthermore, to trigger a performance failure, current industry standard dictates that the operator must fail the performance test not just once but for multiple years – for two consecutive years in most agreements. Again, this is viewed by the operator as a form of protection in case there is an event that impacts a single year.

The performance test proposed by the majority of operators is so standard, it has become easy to predict its general conditions: the RevPAR index condition will range from 85% to 90%, and the GOP condition will be 85% to 90% of budget. However, by proposing a standardized and predictable performance test, operators fail to duly consider and value the merits of the hotel and the owner’s return requirements.

Another flaw sometimes included in the performance test (typically specified in the term sheet prior to the hotel management agreement) is the failure to determine the competitive set that defines the test’s RevPAR index. This lack means it is difficult – even impossible – for the owner to assess the reasonableness of the penetration percentage.

RevPAR test must relate to operator underwriting RevPAR

Owners must determine if both the competitive set and RevPAR index proposed by the operator are appropriate. To do this, we propose linking the RevPAR test to the operator’s underwriting of the hotel’s operations. For example, at Hotel Asset Value Enhancement, Inc. (hotelAVE), we underwrite the market’s performance and hotel’s anticipated performance based on the positioning of the hotel in the market, as compared to the proposed competitive set, and use that information to determine the appropriate RevPAR index for the hotel and its performance test.

Owners should also compare the RevPAR index proposed for the performance test to the stabilized RevPAR index in the operator’s underwriting. More often than not, a significant gap exists between the RevPAR index proposed for the performance test and the RevPAR index in the operator’s underwriting. In our view, no more than a 10 point discount should occur between the RevPAR index in an operator’s underwriting and the performance test index. As shown in the example in Table 1, the test RevPAR index varies significantly from the underwritten RevPAR index (both the operator and hotelAVE). Based on the underwritten RevPAR index, a more appropriate test is 95% to 100%, as opposed to the 90% proposed by the operator.

Table 1: Example of the RevPAR index

GOP test must be based on underwriting, not the annual budget GOP

The second prong of the standard performance test requires the hotel to generate a GOP that is a specific percentage of the budgeted GOP for a specific year. Here, operators and owners typically differ in their preferences on how this is defined.

Operators prefer that the GOP test be based on the future unknown annual budget. A performance test based on budgeted GOP is a much easier test for the operator to pass, because the operator can use the test to design the annual budget. This creates misalignment with owner interests by incentivizing the operator to propose a conservative budget – even if owner has budget approval.

For one thing, if the operator is performing poorly, the annual budget would most likely reflect that. Furthermore, an operator in danger of failing the performance test and of being terminated may well prepare a budget that is easily achievable and does not reflect the true operating potential of the hotel. This kind of budget creates a self-fulfilling prophecy, wherein the operator’s conservative budget sets the stage for continued under-performance, which in turn may lead to another budget that does not reflect the hotel’s potential, and so on.

In addition, the budget prepared by the operator under these circumstances may deviate significantly from the results detailed in the operator’s underwriting.

The other negative consequence of basing the performance test on budgeted GOP is that the test can cause conflict between the operator, the owner, and the hotel team. In this situation, the hotel team will receive conflicting messages as, on the one hand, the operator guides the team to do just enough to meet the targeted GOP level and, on the other hand, the owner directs the team to generate a GOP level that provides for a certain economic return. These conflicting messages will confuse the hotel team and cause them to lose sight of the overall goal – to manage the hotel towards the owner’s required return.

Underwriting is a factor an owner will have considered when initially selecting the operator for the hotel property – or, indeed, when deciding whether or not to develop a project. By defining the GOP test as a percentage of the operator’s underwritten GOP, the performance test then considers the owner’s return requirements, including whether the owner will be able to pay future debt service.

Analyzing sensitivity of performance tests to owners’ return requirement

Before signing a hotel management agreement, it is critical that the owner assess the profitability of the hotel under a low-performance scenario – that is, a scenario in which the operator just meets the hotel’s performance test threshold – in order to understand the potential impact on earnings before interest, taxes, depreciation and amortization (EBITDA) – what the owner uses to pay debt service and puts in the bank. If the sensitivity analysis shows that the hotel cannot achieve the owner’s required stabilized yield on cost or total capitalization or cannot pay debt service at the performance test threshold, then the test does not work for the owner, and a different performance test is needed.

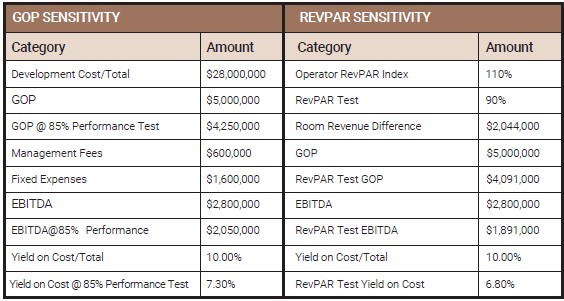

Table 2: GOP and RevPAR sensitivities (assuming a hotel with 140 rooms and a market RevPAR of $200)

As detailed in Table 2, based on the GOP test, the owner’s stabilized yield on cost or total capitalization would be 7.3%, as opposed to a target of 10.0%. Based on the RevPAR test, the stabilized yield on cost or total capitalization would be even lower, at 6.8%. The owner must evaluate if this level of return is acceptable because the owner will be able to terminate the agreement only at performance levels below this return threshold.

Owners should also evaluate whether they can afford the debt service levels and meet the debt service coverage tests with the “poor performance GOP threshold.”

Alternative options for the budgeted GOP test

As detailed in Table 2, the GOP and RevPAR tests do not result in an acceptable return on investment for the owner. Other options to establish a more equitable performance test, and generate a return, include:

- A set hurdle amount tied to a specific economic return – A specific EBITDA amount that generates the required return to the owner;

- Attaining a set GOP margin (as a percentage of total operating revenue) – GOP compared to total revenue as a percentage that would result in an EBITDA level providing for the required return to the owner;

- A percentage of the GOP/NOI levels detailed in the operator’s underwriting – Requiring the operator to achieve a specific percentage of the GOP/NOI detailed in their underwriting.

Hotel management agreement performance tests should allow owners to terminate agreements with operators if the operators underperform. The tests also need to support and align owner and operator interests by factoring in the appropriate competitive set and RevPAR index, as well as the owner’s return requirements. Owners can determine if a performance test supports alignment by running a sensitivity analysis that relates the RevPAR test to the operator’s underwriting and bases the GOP on underwriting instead of the budget.