Our hotelAVE Hospitality Dashboard 3Q25 is now available!

Our hotelAVE Hospitality Dashboard 3Q25 is now available!

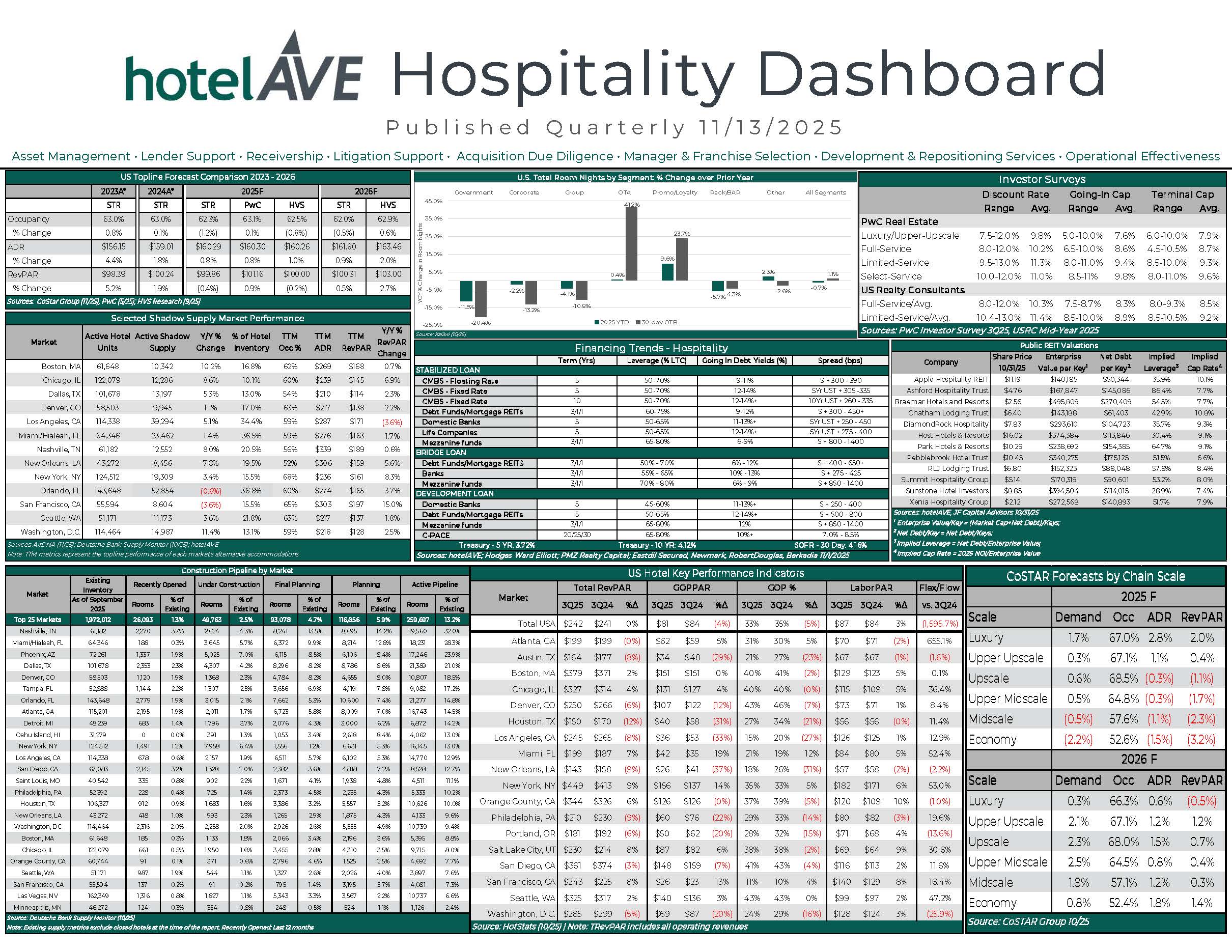

- In October, STR and HVS revised their year-end RevPAR forecasts down further to -0.3% and -0.2% vs STLY. The government shutdown in 4Q25 risks a potentially larger decrease for the full year. 2026 RevPAR growth ranges from 0.6% to 2.7%.

- Corporate, government and group segments continue to be down Y/Y while OTA and loyalty/promotion demand is up Y/Y. The 30 day on-the-books demand for corporate, government and group mirrors year-to-date performance.

- Total RevPAR was negative for most markets in 3Q25 driving GOP margin deterioration.

- Spreads have remained stable since last quarter and banks, debt funds and CMBS remain the most active sources for hotels. Refinancing activity remains robust in a tepid transaction market.

- Despite challenging development yields and softening market fundamentals, recent new openings and projects under construction continue to be added to markets still absorbing 2024 deliveries. In most markets, there are large backlogs of projects in final planning awaiting equity or debt financing. Expect to see some portion of this backlog delayed indefinitely or abandoned as equity sources continue to wait for distress sales.

Download the full summary to stay up-to-date: hotelAVE Hospitality Dashboard 3Q25