Our hotelAVE Hospitality Dashboard 3Q24 is now available!

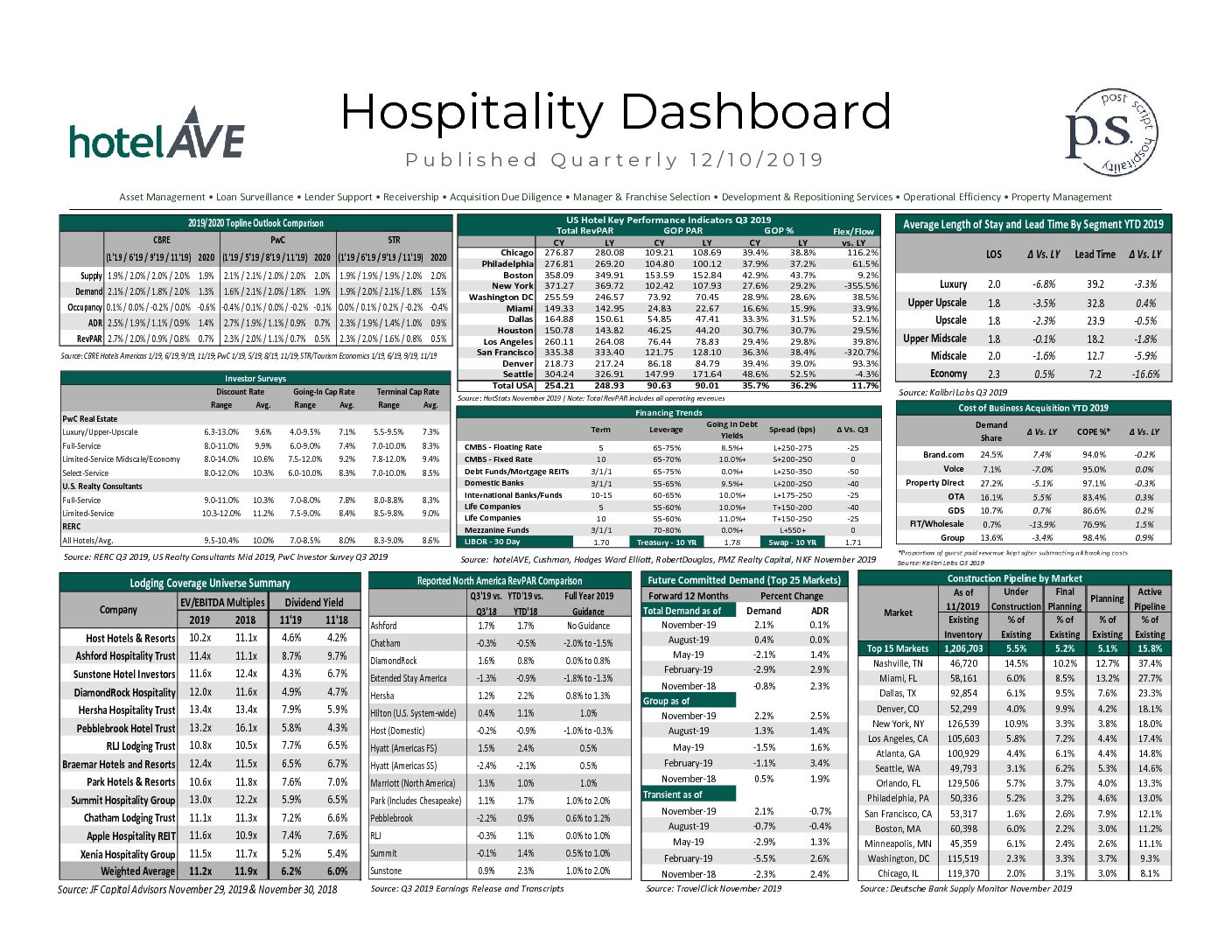

- Q324 Total RevPAR finished up 3% versus Q323, however GOP margins were down 3% or 100 bps. While topline growth was strong across most Top 25 markets, labor costs PAR increased 5% nationally. GOP margins will continue to be stressed by above inflationary growth in labor costs.

- Despite the two recent interest rate cuts, increases on yields of five and ten-year treasuries negated the benefit for fixed rate borrowers. Spreads and debt yield requirements remain stable across various debt sources as market considers how many more interest rate cuts remain.

- 3Q24 growth in OTA, GDS, and Wholesale channels highlight a consumer looking for value; shadow inventory performance reflects this as well. Travelers continue to spend but are searching for deals.

- All categories of the supply pipeline grew versus 2Q24, and total active pipeline is 18.5% higher versus 3Q23. Easing construction backlogs, financing support from lower interest rates, brand concessions and alternative financing sources such as CPACE and EB5 facilitate new starts.

- Transaction market volumes remain muted, weighed down by high bridge interest rates, slowing fundamentals and (mainly defensive) renovation/capital expenditure requirements. Bid-ask spread is causing most owners to refinance versus sell. Business plans with identifiable value creation strategies and brand incentives fuel the institutional grade trades closed this year.

Download the full summary to stay up-to-date: hotelAVE Hospitality Dashboard 3Q24